8

FMI

*

IGF JOURNAL

VOLUME 25, NO. 2

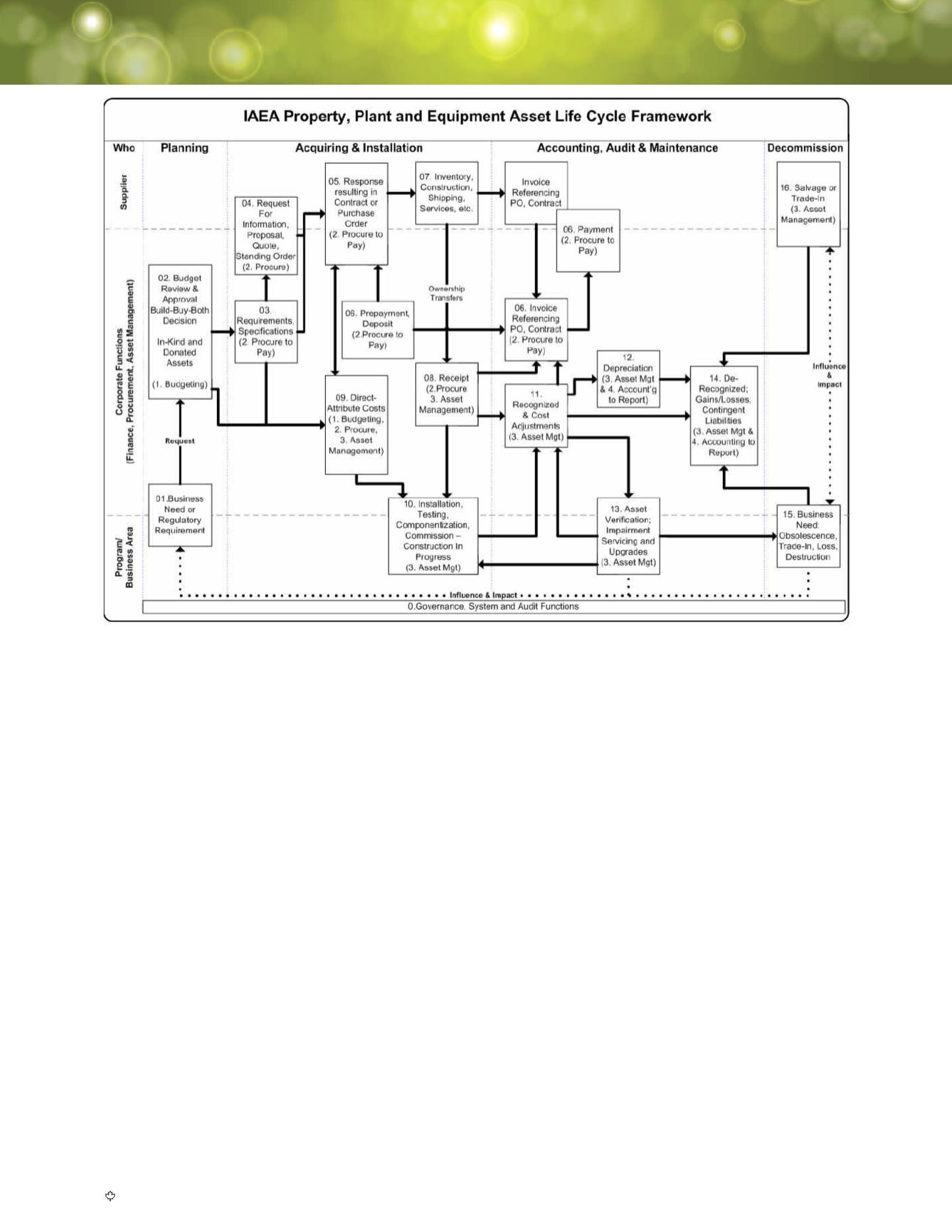

THE INTERNAL ATOMIC ENERGY AGENCY’S PROPERTY, PLANT AND EQUIPMENT (PP+E) LIFECYCLE FRAMEWORK

2.

Procure to Pay:

from requisition

to payment including the treasury

management functions.

3.

Asset management:

the receipt,

installation, maintenance, tracking

and disposal of assets.

4.

Accounting to Reporting:

the

proper accounting, record keeping

and reporting (internal and external)

of assets.

The four horizontal bands identify

the main parties involved in the PP+E

Framework. These are the supplier, the

corporate functions of the organization,

the program or business area, and the

executive or governance function. For

brevity and clarity, the original IAEA

model has been reconfigured slightly.

Generally, an asset will proceed in a

sequential manner from left to right

across the model.

Step 1

Business Need

and Step 2

Budget Review and Approval

• Step 1.

The need to acquire or re‑ invest in an

asset.

• Step 2.

Budgeting request and approval.

Steps 1 and 2 represent central

resourcing and funding questions within

an organization. The IAEA has both

an operating and a capital budgeting

processes. Given the specialized and

technical nature of the Agency, it

often has to consider whether to build

or buy an asset. For Public Sector

organizations, there is also a temptation

to have “Year-End Madness” at this

step; buying frenzies to soak up end of

year budget lapses.

By the completion of Step 2, an

organization knows it needs to buy or

acquire “something” and it has the

money or resources to do so.

Steps 3 – 8

Buying and Paying for the

Asset

Whether buying pens or new jet fighters,

most organizations have a procurement

process represented in Steps 3 through

to 8. The specifications of Step 2 are

refined turning the business need into

approved Step 3 requirements. Buy

decisions continue to Step 4 while build

decisions jump to Step 9.

Step 4, the vendor community bids on

supplying the asset.

Step 5, Vendors respond to the above

request. This will typically create a

Purchase Order or Contract for goods/

services. The successful vendor may

require more (or less) organizational

staff involvement than originally

anticipated. This may change the

expected Direct Attribute Costs of the

asset (more on this in Step 9).

Step(s) 6 are Finance Department

focused. We first encounter Step 6 if

a pre-payment, deposit or retainer is

required.

Step 7; the vendor provides the goods

(or services). (Author’s note, while this

may involve a capital lease from the

vendor, for brevity, this is beyond the

scope of the article).

Under IPSAS, and with Step 8, the

vendor transfers ownership of the asset to

the organization. Previously, Steps 6 and

8 were the end of the IAEA accounting

Figure 2: IAEA’s Property, Plant and Equipment Asset Lifecycle Framework