SPRING 2014

FMI

*

IGF JOURNAL

11

THE INTERNAL ATOMIC ENERGY AGENCY’S PROPERTY, PLANT AND EQUIPMENT (PP+E) LIFECYCLE FRAMEWORK

falls between the minimum floor cost

and the asset capitalization threshold.

The term “for which there is a market” is

what makes the asset attractive. A market

refers to the

relative ease

in which an asset

can be used personally, sold in a white/

grey market (pawnbroker, classified

advertisement); or if there is a black or

illicit market for the item. Relative ease

is constrained by the following:

• Demand for the item.

• Its use outside the organization.

• The ability to track or identify the

property as being stolen.

• The real and perceived administrative

or legal consequences to the individual

(staff member or otherwise) detected

holding or distributing the Agency’s

asset.

SIDE BAR – ASSET

VERIFICATION FRAMEWORK

IPSAS is silent on verification but it

does require assets to be impaired if

the functionality has decreased by a

material amount. Thus, if an asset

is missing, it is impaired. Physical

verification was traditionally the best

way to ensure an asset exists (e.g. go and

kick it). However, what happens when

the asset is intangible or is in a hot room

of a nuclear reactor? This is an ongoing

challenge for most organizations and

the IAEA is no exception.

The author implemented an earlier

version of the Asset Verification Frame-

work in the IAEA in 2011. The basis for

the framework is the principle that in-

ternal control efficiency and reliability

is a function of standardization and au-

tomation. The more standardized or au-

tomated an internal control – the more

reliable it is.

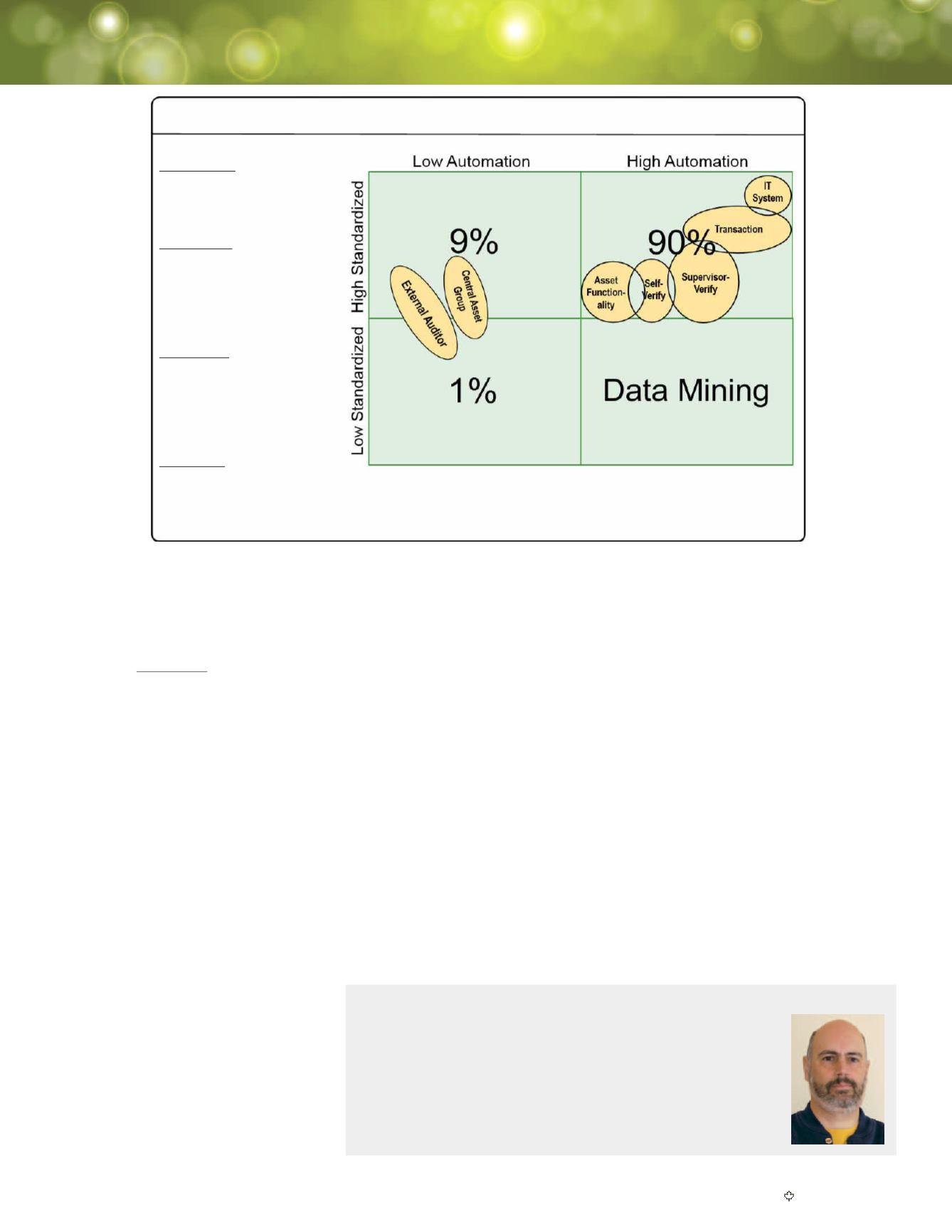

A 2x2matrixmaps these two functions.

Different asset verification methods can

be plotted onto the matrix with the top

right quadrant (high standardization/

high automation) being the sweet spot.

This is not to say the other quadrants

should be empty though; they are still

important as quality assurance methods.

The 90-9-1%+DataMining allocation

is inspired from a similar Social Media

rule of thumb. In this context, 90% of

the social media users will never create

content, 9% will contribute to existing

content but only 1% will actually

create content. Extended to the asset

verification context:

• 90% of the verification activities

should be via highly standardized and

automated means.

• 9% of the verification activities will

contribute to the confidence of the

automated functions.

• 1% of the activities should be used to

audit the other 99%.

• Data mining is not an internal con-

trol but can be used to discover the

“unknown unknowns” about how the

organization buys, uses and manages

assets.

About the Author

Frank Potter is a professional accountant (CMA) and holds a MBA

from the University of Athabasca. He is currently with the Ministry of

Alberta Health and is the Director of Strategic Planning for Information

Management and Technology. Previous to this he has held variety

roles, typically at the Director level, within governmental and consulting

organizations. Contact:

or

.

90% Quadrant:

by asset count or

other measure, conduct about

90% of all asset verifications

here.

9% Quadrant:

used to calibrate and

verify the accuracy and reliability

of the 90% quadrant. About 9%

of all assets should be included

in this quadrant on a periodic

basis (e.g. yearly).

1% Quadrant:

used to ‘discover’

the unusual and outliers. This

quadrant includes external

auditor and internal sampling

(e.g. verification by walking

around).

Data Mining:

Not suitable

as an internal control but

organizational insights may be

revealed through techniques

such as data mining.

The position and size of the various methods are for illustrative purposes only.

The actual placement will vary based on the organization and methods used.

Be sure to visit

for blogs and information about the above methods.

Figure 3: Asset Verification Framework

Asset Verification Framework